Let’s Baby-Proof Your Budget

Welcoming a new addition to your family is an exciting and joyous time. However, it’s also a period that requires careful financial planning. From budgeting to saving strategies and cost considerations, ensuring you’re financially prepared can help secure your family’s future. Learn how to navigate this new chapter with confidence.

Create a Budget

The first part of establishing your budget is to find out where your money goes. Start keeping track of all your expenses over the course of several months. Use the method that works best for you, whether it’s a budgeting app or a spreadsheet. (Download our handy budgeting worksheet here.) If you are a Service Credit Union member, you can use the Money Management tool located under “More Services” in online banking or under “More” in your mobile app to create and keep track of your budget by category.

Now that you have an idea of your spending pre-baby, start to factor in some expenses that are expected after baby arrives: childcare (if applicable), diapers, formula, clothes, etc. Get an idea of what these things cost now before experiencing sticker shock later.

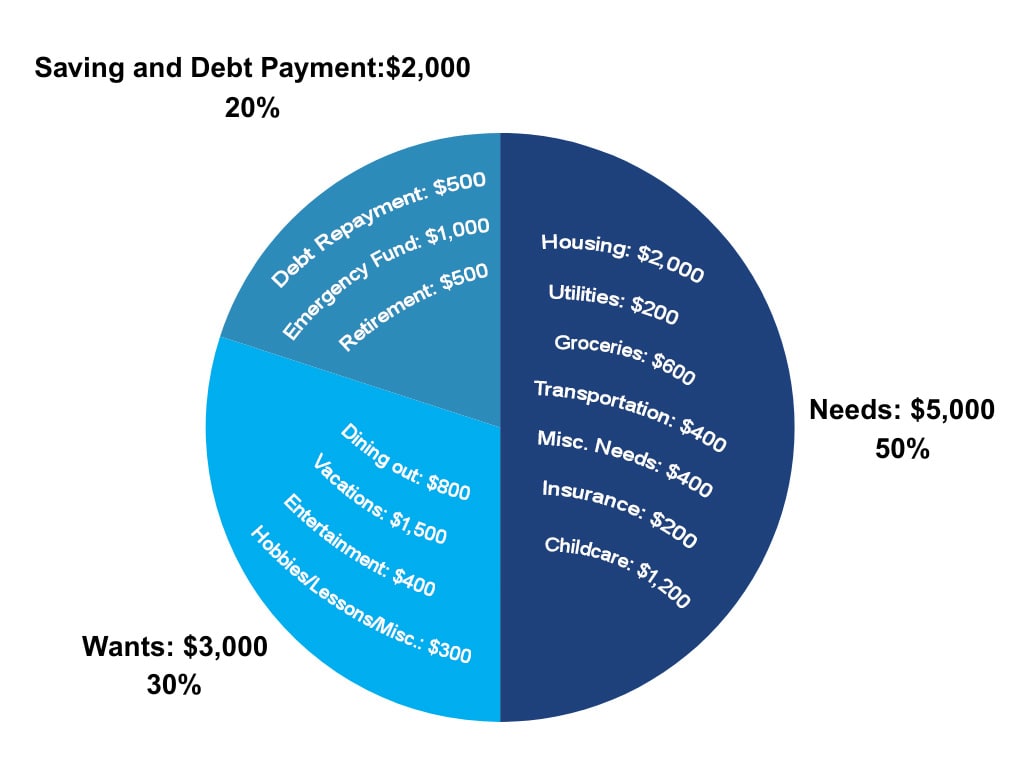

Try the 50-30-20 Rule

This popular budgeting rule suggests allocating 50% of your income to needs (rent/mortgage, groceries, utilities, healthcare), 30% to wants (entertainment, dining out) and 20% to savings and debt repayment. Consider your total household income and re-review your needs list, now with baby items included, to determine how much of your income can be expendable as well as saved. Don’t forget to factor in potential income changes if a parent plans to take extended leave or reduce work hours. If 50-30-20 is not possible, adjust your spending to ensure the “needs” column is being covered.

Here’s a simple example of the 50-30-20 rule being used in a household with a total monthly household income of $10,000.

Looking to make putting aside money easier? Sign up for our high-rate savings account and automatically transfer money into your savings account every month using online banking.

How Much Should I Save Before Having a Baby?

While there’s no one-size-fits-all answer, a common recommendation is to have at least three to six months’ worth of living expenses saved up before your baby arrives. This emergency fund can cover unexpected costs such as medical bills, additional childcare needs, or any unplanned time off work.

Be prepared to spend more than normal in the first few months of baby’s life, when you’ll need to buy a stroller, a crib, car seat, etc. Consider buying used when possible, and get some other great money-saving tips for baby here.

What About a College Fund, and Other Future Considerations?

While college is still 18 years away, if you have the means to put some extra money aside, it doesn’t hurt to start now. Learn more about 529 plans and how they work, including if you need more than one for multiple children, and what happens to them if your child does not pursue higher education.

Now is also a good time to review your life insurance coverage, as well as to do some estate planning. Although putting together a will or a trust is never fun, it should be on your checklist once you have kids.

At this point, you may be panicking about whether you’ll ever be financially secure enough to have a child, but try not to stress out. While your needs vs. wants list may no longer be what it was pre-baby, by getting a grasp of your spending habits now, automating your savings and preparing for the future, you’ll be on the path to having a financially fit family.